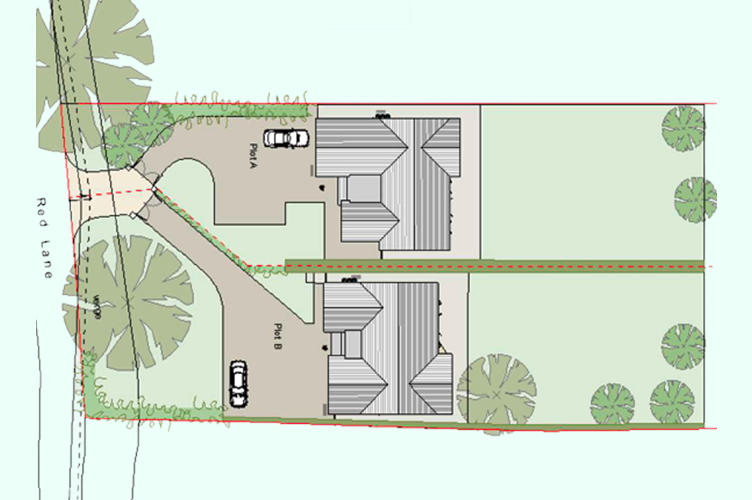

Our borrower had secured an Option Agreement to purchase a disused garage site, with planning in place, at a purchase price of £990,000. Their vision was to demolish the existing garages and build two new family homes, with a projected GDV of £4.15 million.

The vendor, concerned about potential Capital Gains Tax changes in the upcoming budget at the time, pushed to bring the deal forward, requiring the borrower to complete several months ahead of schedule.

To make things more complex, a proposed joint venture with the vendor fell through, leaving the borrower without a funding partner and up against a rapidly closing completion window.

Challenges

1. Tight Deadline

The borrower was already in their notice period and needed to complete urgently after the JV agreement fell through.

2. Planning and Site Constraints

The site had various pre-commencement planning conditions, including demolition constraints, ecological safeguards, and Network Rail requirements due to proximity to the railway.

3. Multi-Party Coordination

The deal required close alignment between valuers, solicitors, quantity surveyors, and our internal funding partners.

Solutions

- Took a commercial and pragmatic view on the planning position, allowing key surveys and reports to be submitted as conditions to drawdown of the development tranche, rather than pre-completion.

- Retained £100,000 on Day 1 to mitigate risk while demolition-related planning conditions were still pending, whilst still releasing sufficient funds to facilitate completion of the purchase.

- Maintained proactive communication between all parties involved, ensuring that, even with a compressed timeline, underwriting, legals, and completion proceeded smoothly.

Outcome

The borrower successfully completed the purchase ahead of the revised deadline and has now started development. The final facility totalled £2.9 million, structured at 63% LTV, 70% LTGDV, and 85% LTC. The two new homes are expected to come to market in a strong residential area with a projected GDV of £4.15 million.

The planned exit strategy is the sale of both completed 3-bedroom houses, with the borrower intending to leverage their strong social media following to drive interest. They have successfully sold previous developments through online engagement and expect a similar outcome for this scheme.